After months of meticulously budgeting and cutting back on lattes, I finally managed to save up enough money to splurge on a deluxe pizza with all the toppings. I was feeling so accomplished that I decided to document this financial milestone on social media, complete with a celebratory selfie holding my pizza like a trophy, capturing the moment I had “made it” financially.

Little did I know, I accidentally tagged my boss in the post, who then promptly thought I was hosting a pizza party at the office. Before I knew it, my coworkers were showing up with a side salad to “balance” the event. So, there I stood with my deluxe pizza, surrounded by colleagues, trying to salvage my “financial victory” while fielding jokes about my new fiscal responsibility: apparently, it included catering duties!

in Funny

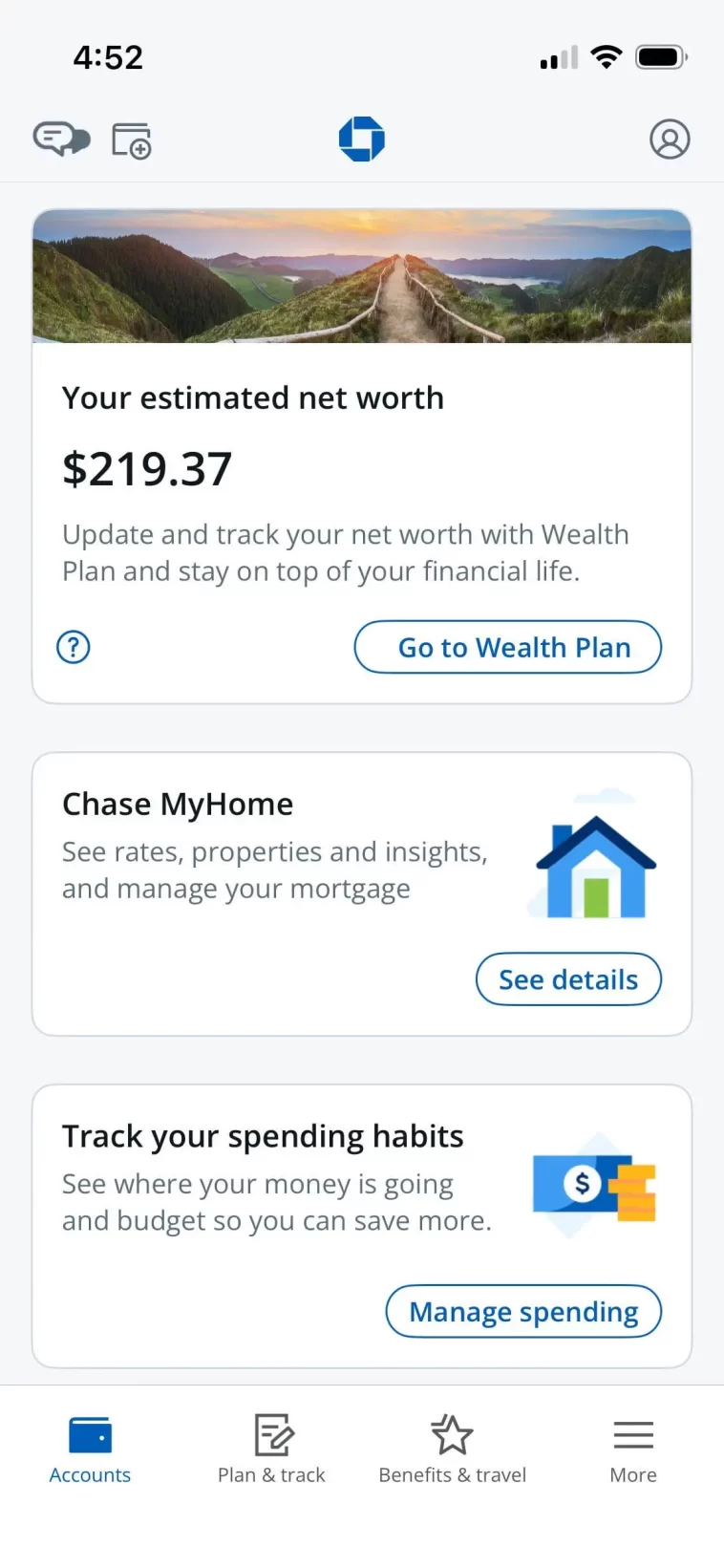

Financial achievement reached.

G

Tbf, if your net worth really is +$219.37, youre probably doing better than the majority of us with more debt than capital

–

All it takes is one day to scroll through stocks or wsb to think you’re behind if you don’t have $200,000 in savings But yes. no debt means you’re in the upper half

B

If you’re in your late 30’s/early 40’s you absolutely should have $200k+ in retirement.

G

“Should” does a lot of work there, though. The median retirement saving for a 40 year old American as of 2 years ago was roughly $45,000. Which obviously means that half of 40 year old Americans have less than that. And most of the half that have more will still have less than $200k+

J

It really depends on how you are structuring your retirement. I made the decision, which has worked very well for me, to focus on having my house paid off. Today I have a net worth well over $1M and with a house that’s paid off, I can retire with my single largest monthly expense not being housing.

G

I mean, this is really context dependent, and I’m not sure what you mean by “structuring your retirement”. If you have a low mortgage interest rate locked in, putting your savings in low cost index funds will almost always have a better return than paying extra on your mortgage. If you are stuck with a high rate due to rates being high the last few years (or other periods in the past), it makes a lot more sense.

J

I forget the rate because that loan was originated 20+ years ago, but I’m referring to just sticking to paying off the mortgage. Some people would rather own their house the day they retire so they aren’t paying a mortgage out of retirement money. Since the imputed income value of a mortgage-free house isn’t income it doesn’t affect your taxes or what you pay for Medicare. The net result is being able to retire on far less income, and that’s independent of what the market does. Right now, if I retired tomorrow, my SS payment is more than average monthly expenses without touching anything else. So, I don’t have to take anything out until RMDs would kick in. At which point I can just invest that money and let it keep growing along with the extra money from Social Security.

I

The point above was that if your mortgage charges you 2% interest and you can make 4% interest on an investment, you should only make the minimal payments to your mortgage and invest any extra money, because your investment would grow faster than the interest in your mortgage. In 20 years you cash out the investment and pay off your 30 year mortgage faster. If like me you pay 6% on your mortgage and there’s no investment that can reliably make anywhere near that return, you should just pay off your mortgage.

J

That’s the theory, but it isn’t the practice, especially during economic downturns when you are most vulnerable to home loss. My original mortgage was 7.625% for 15 years, fixed. I refinanced it for 10 years at a few points lower, with no equity coming out. I paid it off on time, more or less. I was also very heavily invested in a 401k for the tax leverage. The market tanked and I was unemployed for over 99 weeks. At the same time, home values declined and I had a house with a small mortgage that I could alway liquidate my last remaining 401k to pay off if needs be. The “make minimum payments because money is cheap” approach would have left me with a much larger mortgage and a much higher risk of foreclosure. I’ve run the numbers many times over the last 15 years and the only thing I could have done different was less pre-tax investing, but that would have reduced my tax savings, so who even knows how that would have worked out. There really are other perfectly valid retirement strategies which take into account market risk versus home ownership certainty. Because my largest monthly expense is far below the cost of even a crappy apartment where I live, I have more savings and investment options and I’m in a situation where I can retire tomorrow, live on Social Security and still sock more money away in savings.

T

A lot of these “in theory” posts actually you follow the theory perfectly. In practice I think that people that say their going to save and make min payments under save to what they say, and people working to pay off their mortgage overpay and pay it off faster. You have a million dollar net work, so I think that the proof is in the pudding so to say. Good work

J

A knew a lot of people in my 30s and 40s who did something else bad, which was the made the minimum payments, and they saved … some … but then they did a cash-out refinance and suddenly they were back to owing more than they saved. Just to loop back around to the OP, I didn’t have a non-negative net worth until I was 27. I don’t think my parents had a positive net worth until their 30s. It is a genuine milestone.

M

Our house is paid off, and it’s still our biggest expense after taxes. Oops–that expense is half taxes.

J

My single largest monthly expense is now my property taxes. Food is in close second. But you‘re right – Federal Income Tax is my largest gross income expense. When I was doing the math 25-30 years ago, to make plans to actually retire, one of my concerns was the higher my income in retirement – such as if I had to pay a mortgage – the higher my taxes were. I’ve learned there are issues with just about every valid strategy, such as having so much in a 401k or traditional IRAs that the Required Minimum Distributions can keep your taxes high.

S

I don’t know anyone that has that much saved at that age, including myself

B

I’m a bit over $225k at 42, and my spouse has more than that at 40. I’ve been religiously contributing to a 401k since I was 17. I never made over $55k until my late 30’s. It can be done.

O

Which means you’re probably still negative if you owe $300k+ on a mortgage. Net worth is a fun comparison target, but isn’t really worth much outside that.

C

If you count your mortgage you should count the value of the property as well imo

O

Absolutely. Otherwise just leave both out, since the house is super illiquid, usually.

O

My retirement plan is selling my house and downsizing atm. I have about $300k in equity

M

Oops

D

I always thought the guide line was a years salary saved by 30. Not sure what the average actually is

D

Sure, but $200k in retirement savings + $200k left on the mortgage works out to $0 net worth. Not counting other assets obviously, just demonstrating a point.

F

I’ve got debt but still have a positive net worth. My house is worth way more than I paid for it (which is both good and bad because of taxes) so it’s a net asset. My wife and I also have quite a bit in 401k retirement accounts But we don’t have big cash reserves. I wish we did. It’s easy to do a 401k but cash has a way of disappearing.

J

That’s a dangerous situation to be in because if you need more cash than you’ve got during an economic downturn you can get trapped where you’re forced to live on your 401k, pay the penalty for that privilege, and be selling in a down market. Ask me how I know this.

A

What is the story morning glory? Did you get a taste of the 401k money and get hit with early withdrawal fee and then have to pay it back?

J

No, I was unemployed during the Great Recession. I was 401k-rich and cash-poor. I’d never been unemployed more than maybe 2 weeks, so my emergency fund was only maybe 6 months.

I

Yeah I’m excluding the house from any net asset calculation. That’s not an investment I can sell to cover my living expenses, at least not without really changing my situation for the worse. Here in Australia we also can’t take money out of our equivalent of 401k before retirement age, unless you are either on the brink of bankruptcy or death.

W

Not no debt, even just positive net worth. You can easily have more capital than debt, but having some amount of debt is kinda necessary, even beneficial if you can get loans for below what that same money debt-free would lose in investments. A loan for 6% with your regular monthly payments nets more money overall if you can instead of paying it off in full, have the worth go into an 8% yield investment.

A

\>having some debt is okay if capital is going to make you more money Yeah it’s great until the bubble pops and you lose your job and you have to sell at the bottom to make ends meet! Being debt-free ensures you are not forced to make bad decisions with your finances, not that most Americans could snap their fingers and be out of debt.

M

Yeah net worth is still not the perfect measure but it’s better than saying debt is bad. If you can make 8% on a 4.5% loan you’re ahead. You’ll still have debt but be net positive.

D

Comparison is the thief of joy.

D

>or wsb to think you’re behind if you don’t have $200,000 in savings I mainly see loss porn on WSB, if you have more than $100 / aren’t in the red, you’re probably ahead of more than half of wsb 😂

H

Honestly scrolling thru wsb makes me feel better sometimes. Some of those dudes gamble and lose way too much on options.

M

Debt isn’t bad. But no assets with debt is bad.

D

This calculator doesn’t seem to take into account exterior debs from chase. It says my net worth is about $16K (which is what is in my savings + checking account). But I have about $20K in student loans and $25K car loan so my net worth is effectively negative.

G

No, it only includes chase accounts as far as I know

R

It would only know the rest of your financial picture, if it had a way to import that and you made the choice to do so.

T

I agree. I guess whoever posted this doesn’t understand finance. Id kill to have a positive net worth. But some way to go.

D

Kill to have a positive net worth 📝🤓

Y

Clippy popped up at the right time. “It looks like you’re contemplating murder for financial gain. I can help with that.”

B

I didn’t even know this was an option until now!

F

Is your business murder as well?

N

Murder Inc

E

Do people realize the rich operate on a substantial amount of debt with paper wealth that’s based on stocks which oftentimes have zero real monetary value?

B

Maybe whoever posted this is saying just that. They could have paid off all their debt, or at least have less debt than assets.

M

$219.37 is five figures, so pretty good.

R

Yeah, Mr. positive number showing off over there

A

Yeah my net worth was like -$200k last year. I’ve worked my ass off this year and brought it up to -$100k. Winning!

R

Not going to look up or verify but a few days ago I saw someone say around 1/3 of American adults have negative net-worth due to credit card debt, student loans, etc. (mortgages don’t count unless what is owed is more than the value of the house).

B

yeah I was going to say that if you just recently went from -500 to +200 that is a cause for celebration.

GIPHY App Key not set. Please check settings